Views

Making Every Proxy Vote Count Through a Connected Infrastructure

Proxy voting is central to how shareholders influence the companies in which they invest. Each year, investors use proxy votes to weigh in on issues such as board composition, executive pay, capital allocation, climate disclosure and the oversight of emerging technologies. Most of these decisions take place during “proxy season”, the period when annual general meetings (AGMs) are most frequently held, typically in the spring in many major markets including the U.S.A, U.K., Singapore and most of Europe.

In modern capital markets, most investors do not attend shareholder meetings themselves. Instead, they vote by proxy, authorising another party to cast votes on their behalf according to specific instructions or voting guidelines. This system allows millions of shareholders around the world, from large institutional asset managers to individual retail investors, to participate in corporate governance even when shares are held through intermediaries such as brokers, custodians or nominee accounts.

Proxy voting has also become an increasingly visible part of stewardship. Institutional investors may use their proxy votes to signal views on company strategy, risk management, executive remuneration or sustainability issues. At the same time, expectations from regulators, stewardship codes and clients continue to evolve, shaping how asset managers approach proxy voting from one season to the next.

Investor interest in the proxy voting process remains high. A study by Vanguard found that more than 80% of investors believe asset managers should consider their preferences when casting proxy votes, while only a small minority say they would prefer not to participate in voting at all.

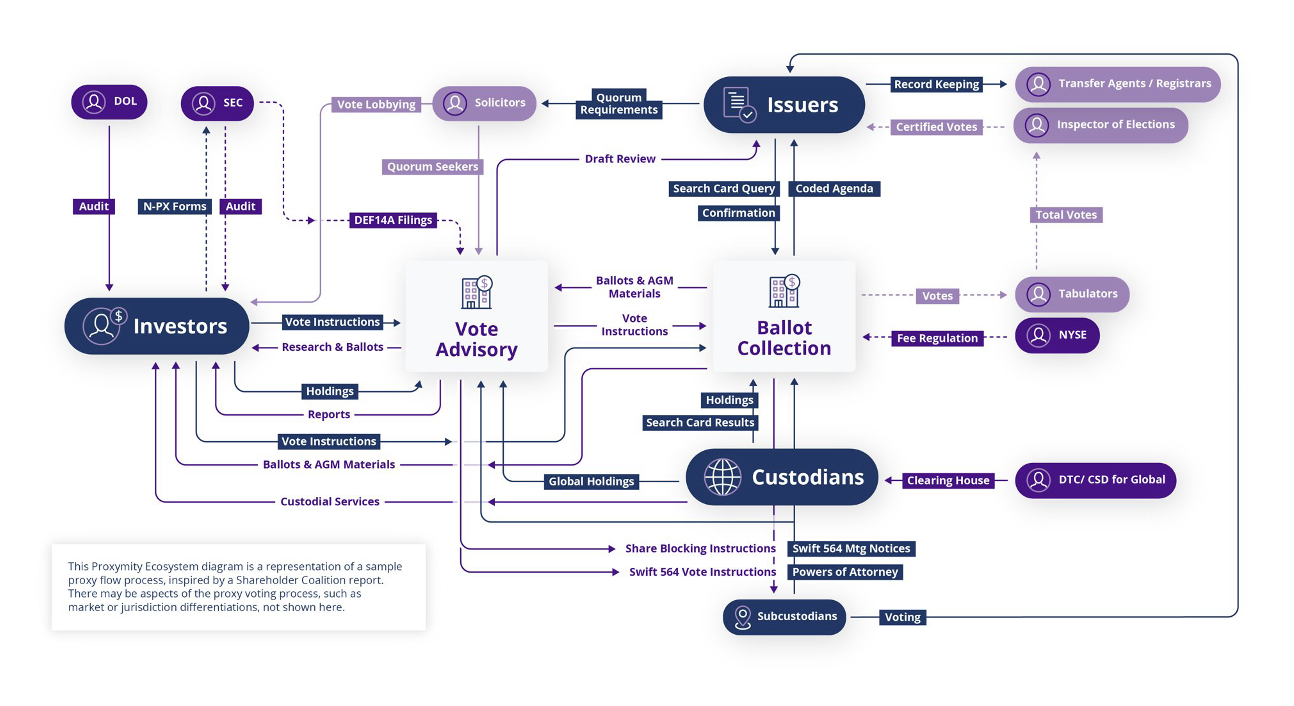

Despite its importance, the operational reality of proxy voting can be complex. A meeting notification or agenda and a single proxy vote may travel through multiple intermediaries, systems and market infrastructures before reaching the issuer or its agent.

As volumes grow, demand for transparency rises and timelines tighten, market participants are increasingly focused on how proxy voting works in practice today, how information moves through the custody chain, and how infrastructure needs to be improved to support more transparent and reliable shareholder voting.

What is a proxy vote?

A proxy vote occurs when a shareholder authorises another party, known as a proxy holder, to cast votes on their shares at a shareholder meeting. Instead of attending the meeting themselves, the shareholder submits voting instructions that determine how their shares should be voted on the agenda items.

In practice, most shareholders do not appear directly on a company’s share register. Shares are often held through brokers, custodians or nominee accounts within the global custody chain. Because of this structure, many investors participate in corporate governance by submitting proxy voting instructions through their intermediary, who then transmits those instructions through the custody network to the issuer’s meeting agent or proxy tabulator.

The proxy holder who formally casts the vote is typically the meeting chair, company secretary, or another authorised representative of the issuer, rather than the investor themselves. The proxy holder votes according to the instructions received from shareholders or their intermediaries.

For institutional investors such as asset managers, proxy voting is closely linked to their stewardship and fiduciary responsibilities. Many institutions establish proxy voting policies or guidelines that determine how their shares should be voted on common issues such as director elections, executive compensation, shareholder proposals, or mergers and acquisitions. These policies may also incorporate research and recommendations from independent proxy advisory firms.

What are the types of proxy votes?

Proxy voting covers a wide range of agenda items that shareholders are asked to decide at company meetings. While the exact structure varies across markets, several common types of proposals typically appear on proxy ballots.

These include:

• Management proposals, such as routine director elections, auditor ratification, or approval of executive compensation

• Shareholder resolutions, which are proposals submitted by investors, often requesting additional disclosures, governance changes, or policy commitments

• Contested votes, such as proxy contests or contested board elections, where different groups actively solicit votes for competing outcomes or director slates

Together, these proposals shape much of the long-term governance relationship between companies and their shareholders.

Beyond the items themselves, there are also different voting instructions and vote standards that influence how outcomes are determined:

• Directed voting: the shareholder instructs the proxy exactly how to vote on each item: for, against, or abstain, for example.

• Discretionary voting: where permitted, the proxy holder may exercise discretion when no instruction is provided or when procedural matters arise at the meeting.

• Abstention: the shareholder chooses not to vote for or against; depending on local rules and company bylaws, abstentions may or may not count towards the vote total.

• Plurality vote: a candidate is elected if they receive more votes than other candidates, even if this does not represent an absolute majority

• Majority vote: an outcome where a proposal passes only if it receives more than 50% of votes cast or, in some cases, of shares outstanding

Across markets, these mechanics are framed by local company law, listing rules, and evolving expectations on stewardship and shareholder rights.

How does proxy voting work in practice?

In modern capital markets, a proxy vote moves through a chain of financial intermediaries before it reaches the issuer. Because many shares are held through custodians, brokers, or nominee accounts, the investor who ultimately owns the shares (the beneficial owner) is often several steps removed from the company itself.

As a result, proxy voting follows a structured process that begins when a meeting is announced and ends when votes are tabulated.

1. Meeting announcement and record date

The process begins when a company announces its shareholder meeting, typically an annual general meeting (AGM) or extraordinary meeting.

At this stage, the issuer publishes its proxy statement (in the U.S) or notice of the meeting (in markets like the U.K, EU countries and Australia), which outlines the meeting agenda, proposed resolutions, and the board’s recommendations.

This step also establishes several key operational parameters:

• Record date: the date used to determine which shareholders are eligible to vote. Investors must hold shares on this date to participate in the meeting

• Meeting details: including whether the meeting will be held physically, as a virtual meeting or in a hybrid format

• Voting deadlines and cut-off times: the latest time by which voting instructions must be received

These details form the foundation of the proxy voting process and must be accurately transmitted through the custody chain.

2. Distribution through the custody chain

Once the meeting is announced, the information flows through multiple market participants. Typically, it passes through:

• Central securities depositories (CSDs)

• Local custodians or sub-custodians

• Global custodians

• Brokers and investment platforms

At each stage, intermediaries distribute the meeting information to the next participant in the chain until it ultimately reaches the investor or the investor’s asset manager.

This distribution process ensures beneficial owners, even when they hold shares through nominee or omnibus accounts, receive the information needed to participate in the vote.

3. Investors review the agenda and decide how to vote

Once investors receive the proxy materials, they review the meeting agenda and evaluate the proposals.

Institutional investors often rely on a combination of:

• Internal stewardship teams

• External proxy advisory research (from the likes of Glass Lewis or ISS)

• Company disclosures and engagement history

• Their own proxy voting guidelines

Based on this analysis, the investor determines how their shares should be voted on each resolution. Evidently, this step requires a lot of research and involvement from various governance teams, as it impacts stewardship at large companies.

4. Voting instructions move back through intermediaries

After making their decision, investors submit voting instructions through the systems used by their custodian, broker, or voting solution, like Proxymity’s Vote Connect Platform.

Those instructions then travel back through the custody chain toward the issuer. Intermediaries must ensure that the voting instructions remain accurate, complete, and aligned with the investor’s holdings as they move through multiple operational layers.

Because each intermediary may apply its own operational deadlines, the cut-off times for investors are often earlier than the issuer’s official deadline.

5. Vote tabulation and confirmation

Finally, the voting instructions reach the issuer’s tabulation agent, which is responsible for counting votes and confirming the results.

The tabulator verifies:

• The number of shares eligible to vote

• The validity of the proxy instructions received

• Whether quorum requirements have been met.

Once the votes are counted, the final results are announced at the shareholder meeting and later published by the company.

Proxy vote examples from recent seasons

Proxy votes often attract significant public attention when they involve large companies, emerging technologies, contentious governance issues or are accompanied by activist campaigns. Recent proxy seasons have produced several notable examples.

• ETF governance debates: In December 2025, a proposal related to the Invesco QQQ ETF drew widespread interest from both retail and institutional investors. The vote demonstrated how decisions involving large index funds can generate significant market attention and debate

• ESG and climate proposals: Proxy voting around ESG proposals are common in markets like the EU. For example, shareholders at Shell’s 2024 AGM voted on the company’s climate transition strategy, reflecting how ESG priorities increasingly shape proxy voting. At the same time, recent seasons have also seen a rise in anti-ESG shareholder proposals

• Technology governance proposals: In February 2025, a shareholder proposal at Apple seeking greater transparency around artificial intelligence practices received roughly 38% support. While the resolution did not pass, it highlighted how emerging technologies are increasingly appearing on proxy ballots

Why proxy voting remains operationally complex?

Although proxy voting is a well-established part of corporate governance, the operational infrastructure that supports it has historically evolved in a fragmented way. In many markets, proxy voting still relies on a multi-layered chain of issuers, intermediaries and investors, each using different systems, data formats and timelines, creating operational challenges even today.

Fragmented infrastructure across the voting chain

Proxy voting information typically passes through several layers before it reaches the end investor.

Each participant may apply their own processes and deadlines. As information is transmitted and reformatted along the chain, inconsistencies can emerge that make it difficult for investors to act quickly or confidently.

In one Proxymity market study on the Australian market, 75% of custodians reported experiencing data leakage or information gaps during proxy events, illustrating how easily information can become distorted as it moves between systems.

Incomplete or inconsistent meeting data

Reliable proxy voting begins with accurate meeting announcements. However, research suggests that key meeting information is not always complete when first distributed.

A Proxymity study on Australia, conducted in collaboration with The ValueExchange found that 24% of meeting announcements contained incomplete information, which may force intermediaries and investors to reconstruct key details before they could begin analysing proposals.

Other findings from the same research showed that only 8% of meeting notifications were published within 24 hours, reducing the time investors had to review materials before voting deadlines.

When essential details such as record dates, cut-off times or voting options are unclear, operational teams must intervene to resolve discrepancies before votes can be submitted.

Manual workflows and operational risk

In most major markets, legacy proxy voting processes still rely on manual workflows and fragmented communication channels.

Earlier industry studies highlighted the widespread use of manual methods such as spreadsheets, email or even fax-based proxy submissions. These processes increased the likelihood of errors and created operational delays as voting instructions were passed through multiple intermediaries.

The complexity of the custody chain also increases the risk of discrepancies in voteable positions. Share ownership may change between the record date and the voting deadline, requiring intermediaries to reconcile holdings across different systems.

These reconciliation challenges can lead to over-voting or under-voting, where the number of votes submitted does not match the number of shares eligible to vote.

Limited transparency and vote confirmation

Another long-standing challenge in proxy voting is the limited transparency available to both investors and issuers.

Historically, many investors had little certainty that their voting instructions had been successfully transmitted through the custody chain or counted at the meeting. Market research conducted found that 75% of investors believed votes were regularly lost or delayed somewhere within the custody chain.

Issuers also faced visibility challenges, with nearly 40% of issuers reporting they were unable to see how beneficial owners had voted. Over 75% said they had no clear view of how long meeting notifications took to reach investors.

This lack of transparency made it difficult for companies and shareholders to engage meaningfully on governance issues ahead of meetings.

Compressed timelines during proxy season

Timing pressure is another defining characteristic of the proxy voting process.

In many markets, companies announce meetings within a relatively short window before the event itself. For example, Australian proxy voting processes have historically operated within a 28-day period between meeting notice and the shareholder meeting, with key operational deadlines (the record date and the proxy lodgement deadline) falling close together.

Intermediaries may also impose earlier internal deadlines in order to process instructions across global custody networks. As a result, investors sometimes have less time than expected to analyse meeting materials and submit voting decisions.

Studies have shown that investors rated their available research window just 2 out of 5 under legacy proxy voting models, reflecting the operational constraints created by fragmented infrastructure and compressed timelines.

Participation gaps across the market

Operational complexity can also affect shareholder participation levels as a result of votes being rejected or missing the deadline.

Market studies have suggested that around 30% of issued capital in large-cap Australian companies is not voted each year. As per some recent analysis by ISS and Sodali & Co, similar outcomes were seen in the UK and European markets.

These gaps highlight how operational barriers and manual processes can limit the ability of some shareholder groups to participate fully in corporate governance.

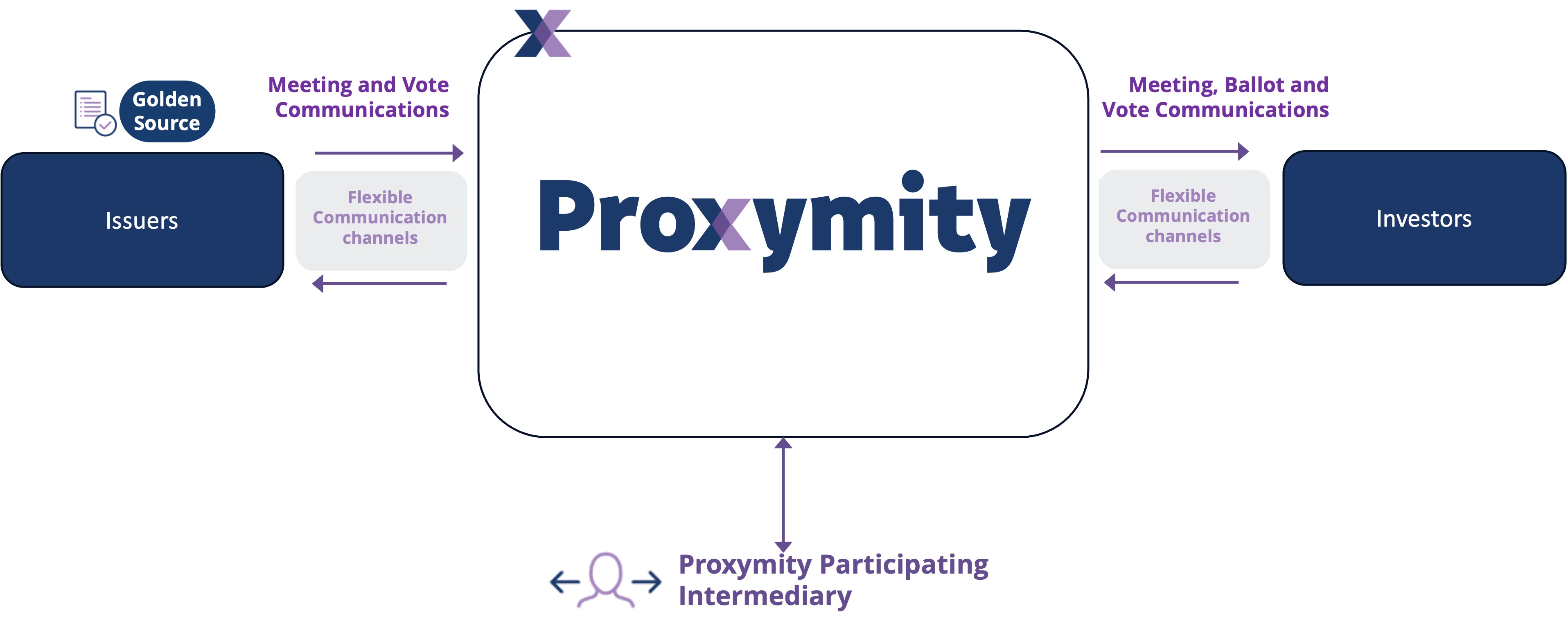

How digitally connected infrastructure is transforming proxy voting

As shareholder participation grows and governance expectations continue to evolve, the reliability of the proxy voting infrastructure itself is becoming increasingly important. Ensuring voting instructions move accurately and efficiently from investor to issuer is essential if every shareholder vote is to be counted.

Prominent market participants, including Deutsche Bank, Euroclear, BNY and TDCC, are exploring digitally connected proxy voting infrastructure to address many of the operational challenges associated with legacy systems. These models aim to reduce manual processing, improve the consistency of meeting data, and increase transparency across the voting chain.

When proxy voting information moves through real-time digital networks rather than fragmented communication channels, participants can benefit from clearer data and more aligned timelines. Investors have more time to analyseproposals and submit instructions, while issuers may receive earlier visibility into voting activity ahead of the meeting.

Studies of modernised proxy voting models have shown that investors can gain several additional days per meeting to analyse and submit votes, while issuers benefit from earlier insight into shareholder participation and voting trends.

Platforms such as Proxymity’s Vote Connect and Shareholder Insights are examples of how markets are enabling structured digital engagement, automated reconciliation and end-to-end vote confirmation between market participants.

Explore a real-world proxy voting transformation

To see how connected infrastructure is reshaping proxy voting in practice, explore our Australia market case study, which examines how digital proxy voting models have addressed long-standing operational challenges and improved transparency across the voting chain.

Other frequently asked questions (FAQs) about proxy voting

Who can be a proxy holder?

A proxy holder is the person authorised to cast votes at the shareholder meeting.

In many cases, shareholders appoint the meeting chair or another company representative as their proxy holder. This person then votes according to the shareholders’ instructions submitted through proxy voting systems.

Investors can also appoint another individual or representative as their proxy holder, depending on the rules of the company and the relevant market.

What is the difference between a proxy vote and a direct vote?

A direct vote is cast by the registered shareholder in their own name. This typically happens when an investor is listed directly on the company’s shareholder register.

A proxy vote, by contrast, is submitted through a proxy holder who attends the meeting and casts the vote on behalf of the shareholder. Proxy voting is particularly common when shares are held through custodians or nominee structures.

What do shareholders vote on during proxy voting?

Shareholders vote on a range of corporate governance and strategic matters during company meetings. Common voting items include:

• Election or re-election of board directors

• Executive compensation and “say-on-pay” votes

• Appointment of auditors

• Shareholder proposals related to governance, strategy, or disclosure

• Capital structure changes such as share issuances or mergers

These votes allow shareholders to influence key decisions that shape a company’s direction and governance practices.

What is the record date in proxy voting?

The record date is the date used to determine which shareholders are eligible to vote at a particular shareholder meeting.

Investors must own shares on the record date to participate in the vote, even if they sell those shares before the meeting itself.

Because shares may be held through intermediaries, determining vote eligibility can require reconciliation across the custody chain.

What is a proxy voting deadline?

The proxy voting deadline (sometimes called the proxy lodgement deadline) is the latest time by which voting instructions must be submitted before a shareholder meeting.

In practice, investors often face earlier deadlines set by custodians or intermediaries to allow time for vote processing through the proxy voting chain.

Why is proxy voting important for corporate governance?

Proxy voting allows shareholders to influence how companies are governed without needing to attend meetings in person, enabling them to express their views on board composition, executive pay, corporate strategy and sustainability issues.

For institutional investors, proxy voting is also an important part of their stewardship and fiduciary responsibilities to underlying clients.

What is a beneficial owner?

A beneficial owner is the individual or institution that ultimately owns shares in a company, even if those shares are held through an intermediary such as a broker, custodian, or nominee.

In proxy voting, the beneficial owner has the right to decide how the shares should be voted by submitting instructions through the custody chain.

While this structure is common globally, there are market nuances. In the U.S., most investors hold shares in “street name” through brokers. In the U.K., EU, and Australia, shares are also commonly held via nominee or custodial accounts, meaning the beneficial owner is typically not listed directly on the company’s share register.