Views

10 Signals That an Activist Investor Wants to Engage Early

When an activist investor goes public, months of preparation sit behind that announcement. The co-investors are briefed. The communications playbook is ready. For most boards, the announcement is the first signal that these investors want to engage with them.

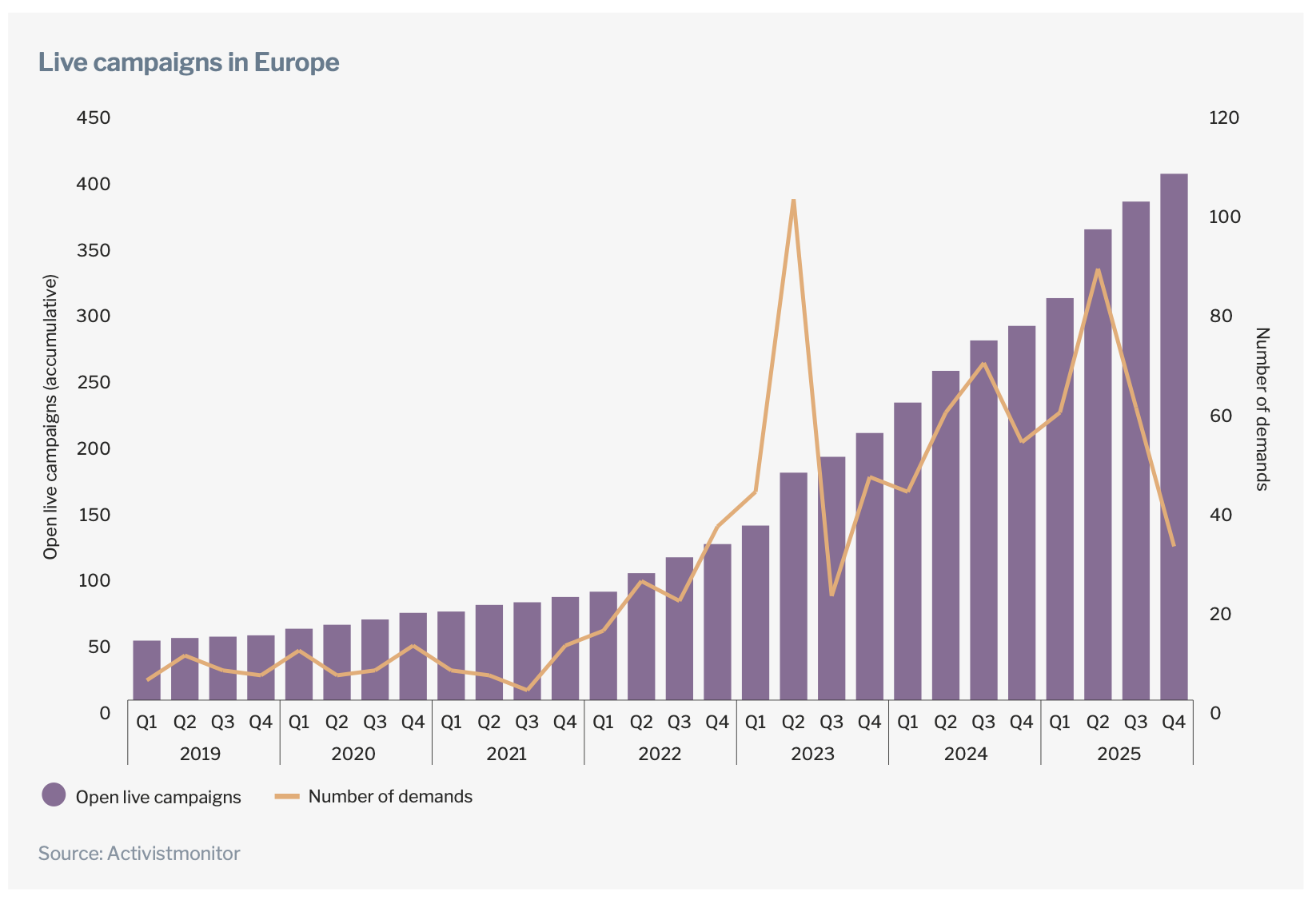

In 2025, activists launched a record 255 campaigns globally. Two-thirds of those campaigns came from first-time activists.

In Europe alone, activists launched 116 new public campaigns in 2025, 43% more than in 2024, according to Skadden’s Activist Investing in Europe 2026 report.

Regulatory filings like 13D, or TR-1 in the UK, tell you a threshold has been crossed. It does not tell you what has been building behind it. By that point, an investor has typically been building their position for months.

This article sets out the signals that appear before the filing which indicate that a shareholder wants to engage early. The ones most boards miss. If you can identify them before, you still have time to engage meaningfully with your investors.

Why do the signals get missed?

Regulatory disclosures exist to create transparency in public markets. For investor relations (IR) teams, they are a useful tool, but not a complete, up-to-date picture. Here is why relying on them alone leaves a gap.

Activist investors generally remain below the threshold

In the US, a 13D filing is triggered when an investor crosses 5% ownership. In the UK, the equivalent TR-1 filing is triggered at 3%. Both thresholds sound low. A potential activist investor can accumulate a significant economic position and influence over fellow shareholders while staying under both.

They do this over multiple quarters, across multiple vehicles. Equity positions move slowly. Derivatives move faster and are not always identified.

Derivatives widen the gap further

Call options and total return swaps give an investor economic exposure to the stock without appearing on the share register at all. The 13F filings that would reveal these positions are published quarterly, with a lag of up to 45 days after the quarter closes. By the time that data surfaces, months have been lost to prepare and engage with investors.

The SEC tightened the 13D window in 2024, but not enough

The window to file after crossing 5% shortened from ten calendar days to five business days. In those five days, investors can buy more shares, brief the press, and connect with your top institutional holders. The filing announcement does not interrupt the campaign.

And the number of companies facing this is growing.

If engagement fails after a 13D or TR-1 is filed, it could push unhappy investors to a proxy contest, a direct campaign to win shareholder votes against the board’s recommendations. At that stage, the company is no longer managing a signal. It is managing a public battle.

10 signals that an activist investor requires early attention and engagement

US activist campaigns jumped 23% year-on-year in 2025. One in six S&P 500 companies currently has an activist on its register, according to Goldman Sachs. Yet the number of campaigns launched by traditional activist hedge funds remains small relative to the pool of companies that fit their target profile.

What IR teams encounter far more often is harder to read: a sense that someone is building interest, without anything yet showing up on the shareholder register. These are the signals worth knowing before a position or a campaign becomes public.

1. An unfamiliar name appears on your share register

New institutional names on a register are not unusual. What demands your attention is a name that appears across multiple consecutive quarters, accumulates steadily, and stays just below the relevant disclosure threshold. That pattern might not be accidental. Cross-reference any unfamiliar holder against known activist fund databases and sector-specific screens. If you see a pattern appearing, it means an investor is looking to engage with the board early and meaningfully.

2. A known passive filer upgrades from a 13G to a 13D

In the US, a 13G signals passive investment intent while a 13D signals the opposite. When a holder already on your register makes that switch, it could signal potential activist activity. Your engagement window from that point could get narrow, and the investor may have been forming views or building intent longer than you think. How you engage with them in the first few days can influence long-term support towards the board’s plans.

3. Unusual options or derivatives activity in your stock

A spike in call option volume or total return swap activity in your stock can indicate that someone is building economic exposure ahead of any formal equity position. Because 13F filings that capture derivative holdings publish quarterly with a lag of up to 45 days, this activity may be visible in market data long before it appears in any regulatory document. Your trading desk, brokers, or specialist analytics provider can surface these patterns, which can go unnoticed by IR teams.

4. The tone of shareholder engagement shifts

Institutional shareholders always ask questions to understand their derived value in holding your stock. What warrants closer attention is the nature of those questions. If your investors seem to be a lot more interested in the following areas, it can be a sign that need a special engagement approach:

• Capital allocation discipline

• The rationale for holding cash

• Stock price relative to its 52-week high and low

• Board tenure and independence

• Executives’ pay relative to total shareholder return

Activist investors look closely at stock prices relative to 52-week highs and lows when screening targets. A stock trading near its 52-week low signals a period of underperformance and an investor who keeps returning to that point in conversation is testing whether management has a credible explanation for it, or whether the gap between current price and perceived value is something they can build a thesis around.

A cluster of such questions arriving from multiple holders in a short window, or escalating in sharpness across consecutive calls, signals a need for more proactive engagement.

Pay attention to what your top holders are asking and track how that changes quarter to quarter.

5. A campaign launches at a sector peer

Investors often build their investment portfolio around sectors rather than individual companies. An activist campaign at a direct competitor or peer is a meaningful signal that the same arguments about valuation, capital efficiency, or governance may already be tested against your own profile.

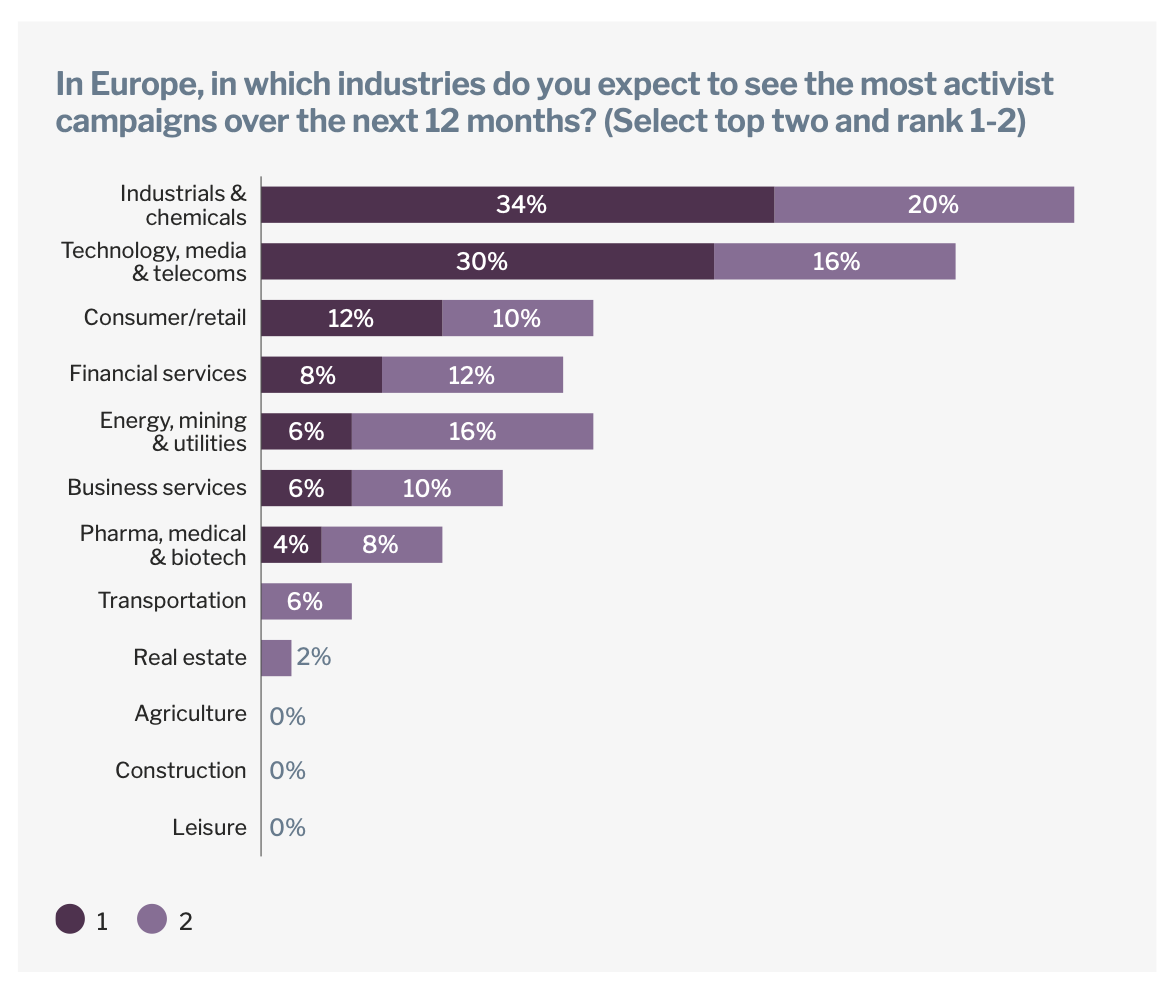

A recent Skadden study identifies industrials, chemicals, technology, media, and telecoms as the European sectors most likely to face shareholder activism in 2026.

If your company sits in one of those sectors and a peer comes under pressure, treat it as a prompt to run your own vulnerability assessment before someone else does and take it as an opportunity to engage with investors meaningfully to understand their preferences and ideas.

6. Your stock appears on activist screening tools or vulnerability lists

Before the point of running an activist campaign, investors run quantitative screens across large universes of listed companies, filtering for:

• Undervaluation relative to peers

• Excess cash with no clear deployment plan

• Sustained underperformance on total shareholder return

• Governance structures that suggest a board unlikely to resist pressure

Several data providers publish versions of these screens publicly. FTI Consulting publishes a quarterly Activism Vulnerability Report that ranks industries by exposure. Diligent Market Intelligence provides ongoing monitoring of activist positioning and vulnerability indicators. Goldman Sachs Research publishes periodic lists of stocks it identifies as susceptible to activist campaigns based on sales growth, EV/sales multiples, and trailing performance relative to sector peers.

If your stock appears on any of these, assume that funds are seeing the same data points and could be concerned or interested in engagement.

7. An unfamiliar fund requests an introductory meeting

Not every activist engagement begins with a visible position on the share register. Some investors initiate informal contact first through introductory calls, strategy discussions, or routine investor relations outreach.

While a normal practice, when an unfamiliar fund with a history of activism begins asking detailed questions around capital allocation, governance, portfolio structure, or shareholder returns, it can warrant closer attention particularly if similar themes are emerging across other investor interactions.

Before engaging, IR and governance teams should review the fund’s historical campaigns, public filings, sector focus, and prior engagement patterns with other issuers. Early conversations are often part of a broader process of information gathering and thesis development.

8. Financial journalists start asking questions about your company

According to Harvard Law School’s guidance on dealing with activist investors, companies can learn for the first time that an activist has taken a stake by reading about it in a news story. By that point, the narrative is already in motion.

Media activity is a standard part of how activist campaigns develop. Research into activist tactics shows that publicity campaigns, including press releases, public letters, and social media, feature in 40% of campaigns. Journalists covering governance, M&A, or capital markets can signal potential activist campaigns.

A cluster of inbound enquiries probing strategy, board decisions, or executive pay should be shared with the investor relations team immediately. The pattern across multiple enquiries matters as much as the content of any individual call.

9. Unusual traffic to your investor relations pages

Your IR website is often the first port of call for anyone conducting structured research on your company. A spike in traffic to specific pages (governance documentation, board biographies, annual reports, capital allocation disclosures) can indicate that someone is building a detailed picture of your business before making any formal approach.

This signal requires a baseline to be meaningful: IR teams that monitor web analytics regularly will spot the anomaly; those that do not will miss it entirely. Work with your digital team to establish what normal looks like, so that unusual patterns become visible when they appear.

10. New or unknown parties attending earnings calls or webcasts

Earnings calls give any listener direct access to management’s narrative, their responses under pressure, and any inconsistencies between stated strategy and reported performance.

Investors building a thesis on your company will often attend several calls before taking any action, stress-testing management’s narrative, identifying weaknesses, and gauging how the board responds under pressure.

Review attendee lists after each call and cross-reference any unfamiliar names against your known investor base. A new attendee asking pointed questions about capital allocation or strategic direction warrants the same follow-up as any other signal on this list.

What to do when you identify these signals

Spotting the signals is only useful if your organisation responds to them at the right time and in the right way.

IR team: act before the picture is complete

Map the shareholder base immediately. Do not wait for a regulatory data set or a second signal to confirm the first. Understand who is building a position, in which markets, and at what pace.

Proxymity Shareholder Insights gives boards and IR teams real-time, accurate beneficial owner data with initial reports available within ten minutes of a request being distributed, so the analysis does not have to wait on manual processes that take days to return results.

Alongside ownership data, Proxymity Vote Insights lets you see how investors are voting in real-time prior to a meeting deadline, and review voting patterns from past meetings. Shifts in how key holders vote on governance or remuneration resolutions, even before any activist position is declared, can be an early indicator of changing sentiment. Cross-reference both of these data sets against known activist screens and your own vulnerability profile to build a complete picture.

Critically, flag the situation to the Company Secretary and CFO before you have all the answers. Early communication inside the business is better than a complete shareholder analysis that arrives too late to other stakeholders.

Company Secretary and General Counsel: prepare the board

Shareholder activism preparedness is as much of a governance issue as it is an IR one. The board needs to understand the company’s exposure and reach alignment on the strategic narrative before an activist tests it publicly. A board that cannot articulate a coherent position on capital allocation or executive pay in a calm setting will not find it any easier under pressure.

You should review takeover defence posture and governance documentation now. Gaps that look minor in normal conditions become material when an activist starts presenting them to your institutional shareholders.

Board and senior leadership: own the investor relationship

Connect with the activist and other key investors before things escalate. Proactive shareholder engagement with your existing investor base is the most effective thing a board can do, not just when signals appear, but year-round.

Commission an independent vulnerability assessment, if not done already. Understanding the gaps in valuation, governance, capital allocation, or board composition gives you the opportunity to address them on your terms.

Across all levels: document everything

If a campaign does go public, your response window is extremely narrow. A clear internal record of when each signal was detected and what actions followed protects the board and the company’s image, as well as aids in creating a more focused, informed response.

The foundation is shareholder intelligence; the best course of action is year-round engagement

Every signal in this article points to the same underlying problem: a company that does not know its shareholder base well enough to spot when it is changing.

The most effective response to that problem is not reactive monitoring. It is year-round engagement; knowing who holds your stock, understanding how they vote, and maintaining consistent dialogue before any external pressure arrives.

Proxymity Shareholder Insights Suite gives IR teams a current, accurate picture of their beneficial owner base and their preferences in real time. That visibility supports ongoing engagement, not just a crisis response during a meeting. Detection is a data problem. Year-round engagement is the best answer to it.

Talk to our experts to learn more about how Proxymity Shareholder Insights helps IR teams stay ahead of potential activist campaigns.

Frequently asked questions (FAQs) about activist investors

What is an activist investor?

An activist investor is a shareholder, typically a hedge fund or institutional investor, who acquires a stake in a public company to influence its strategy, governance, or capital structure. Unlike passive investors, they engage with boards, management, and other shareholders to push for changes they believe will improve shareholder value.

Are activist investors good or bad?

Neither, as a rule. Activist investors hold boards accountable, push for capital discipline, and often drive changes that benefit all shareholders. Some campaigns create short-term pressure that conflicts with long-term value creation. The outcome depends on the activist’s thesis, the company’s circumstances, and how both sides manage the engagement.

How do activist investors work?

An activist investor builds a stake in a company they believe is undervalued, then engages with management to push for specific changes: a strategic review, capital returns, board changes, or asset disposals. If private engagement fails, they go public: launching a campaign, seeking board seats, or putting resolutions to a shareholder’s vote.

Do activist investors add value?

Research frequently shows positive short-term market reactions to activist campaigns, though evidence on long-term value creation is more mixed. Whether those gains sustain is more contested. What is consistent is that activism tends to accelerate decision-making at companies where management has been slow to act.

What are activist investors paying attention to?

Activists screen for companies where the gap between current performance and potential value is large. Key inputs: stock price underperformance versus peers, excess cash, governance weaknesses, executive pay misaligned with shareholder returns, and strategic decisions they believe have destroyed value.

How big a stake does an activist investor need?

Smaller than most boards assume. In the US, a 13D filing is required at 5% ownership. In the UK, a TR-1 is triggered at 3%. But activists routinely influence outcomes with stakes of 1% to 2%, building coalitions with other shareholders to amplify their position and using derivatives that can increase economic exposure while reducing immediate visibility on the share register.

What is the difference between a 13D and a 13G filing?

Both are triggered when a US investor crosses 5% ownership. A 13G signals passive intent holding for investment purposes only. A 13D generally signals that the investor may seek to influence or engage with the company.

Is a passive investor ever a precursor to activism?

Yes. A fund may file a 13G to establish a passive position, then upgrade to a 13D once they have built their thesis and identified co-investors. A long-standing passive holder who begins engaging more actively, asking sharper questions, or quietly increasing their position warrants closer attention.

What should a company do when it first suspects an activist is circling?

Companies should begin assessing ownership patterns and engagement signals early, rather than waiting for formal regulatory disclosures. Cross-reference unfamiliar names against activist fund databases and brief the Company Secretary and CFO early. Do not wait for a regulatory filing to confirm what trading patterns and engagement shifts may already be signalling.